Launching a Fintech savings and investment app called Jollof+ for Baobab Microfinance bank (5 mins read)

Launching a Fintech savings and investment app called Jollof+ for Baobab Microfinance bank (5 mins read)

👋🏽 Introduction

👋🏽 Introduction

In 2023, Baobab Microfinance Bank approached Enyata with an ambitious mission: “Can we help Nigerians stay ahead of the inflation curve by giving competitive interests on savings and investments”

They had the vision, the reach, and the data. But they needed a digital experience that spoke the language of trust, simplicity, and everyday life. That’s where I came in.

In 2023, Baobab Microfinance Bank approached Enyata with an ambitious mission: “Can we help Nigerians stay ahead of the inflation curve by giving competitive interests on savings and investments”

They had the vision, the reach, and the data. But they needed a digital experience that spoke the language of trust, simplicity, and everyday life. That’s where I came in.

My Role

My Role

Lead designer

Lead designer

Interaction designer

Interaction designer

Visual designer

Visual designer

Prototype

Prototype

Platforms

Platforms

iOS

iOS

Android

Android

Web

Web

Year

Year

2023 - 2024

2023 - 2024

❗ The Problem

During our research we identified 4 primary problems with the digital saving culture in Nigeria.

💔 Trust Issues

Many users are wary of saving apps. “What if my money disappears overnight?”

💸 Inconsistent Income

It's hard to set a monthly goal when your income isn’t steady or arrives on set days.

🧠 Overwhelming Interfaces

Most fintech apps are built for people with stable salaries and financial knowledge. We had to start simpler.

💰 Low Incentives

Many users ask, “What’s in it for me?” and rightly so. To build trust and motivate savings behaviour, Baobab prioritised high-interest rates as a key part of the Jollof+ value proposition. This gave users a compelling reason to start and keep saving, with visible returns that reinforced trust.

🎯 Opportunity

🎯 Opportunity

How might we help Nigerians save money in a way that feels safe, easy, and made for their everyday lives?

How might we help Nigerians save money in a way that feels safe, easy, and made for their everyday lives?

🔎 Research and Discovery

🔎 Research and Discovery

Before sketching a single screen, we needed to understand how Nigerians actually think about saving money especially those with irregular incomes.

Before sketching a single screen, we needed to understand how Nigerians actually think about saving money especially those with irregular incomes.

What we did

What we did

• Conducted user interviews with 20+ individuals across Lagos, Abuja, and Ibadan, covering traders, gig workers, and salaried employees.

• Ran a competitive audit of existing savings apps including PiggyVest, Cowrywise, and Kuda to understand patterns, friction points, and trust signals.

• Mapped out two core user journeys: a first-time saver and a returning user managing multiple savings goals.

• Held stakeholder workshops with the Baobab team to align on business constraints, compliance requirements, and interest rate positioning.

• Conducted user interviews with 20+ individuals across Lagos, Abuja, and Ibadan, covering traders, gig workers, and salaried employees.

• Ran a competitive audit of existing savings apps including PiggyVest, Cowrywise, and Kuda to understand patterns, friction points, and trust signals.

• Mapped out two core user journeys: a first-time saver and a returning user managing multiple savings goals.

• Held stakeholder workshops with the Baobab team to align on business constraints, compliance requirements, and interest rate positioning.

ℹ️ Key insight

ℹ️ Key insight

Users didn’t distrust saving, they distrusted apps. The barrier wasn’t motivation; it was credibility.

This insight shaped every design decision that followed, from the onboarding flow to the way we displayed interest rates.

Users didn’t distrust saving, they distrusted apps. The barrier wasn’t motivation; it was credibility.

This insight shaped every design decision that followed, from the onboarding flow to the way we displayed interest rates.

✅ The Solution

✅ The Solution

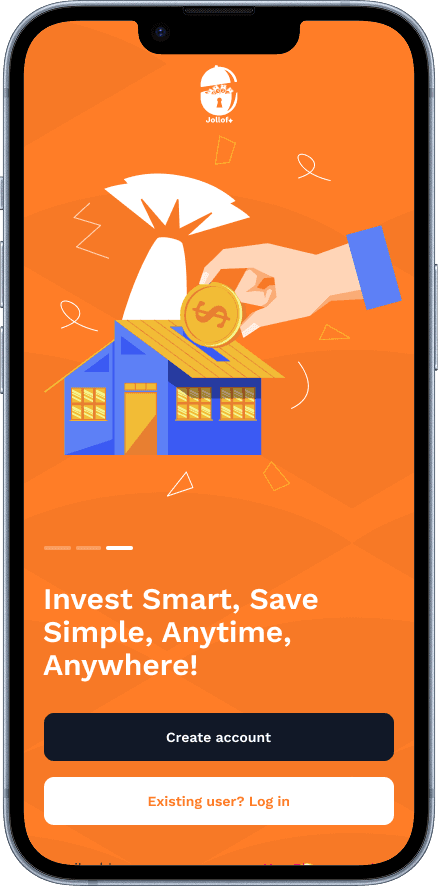

We didn’t set out to build just another savings app. We wanted to create something that felt trustworthy, flexible, and truly Nigerian, built for the way people actually live and earn.

We didn’t set out to build just another savings app. We wanted to create something that felt trustworthy, flexible, and truly Nigerian, built for the way people actually live and earn.

Trust first

Trust first

We led the onboarding with Baobab’s NDIC insurance badge, CBN licensing details, and a plain-language explanation of how funds are protected. By addressing trust before asking for a single naira, we reduced drop-off at the most critical stage of the funnel.

We led the onboarding with Baobab’s NDIC insurance badge, CBN licensing details, and a plain-language explanation of how funds are protected. By addressing trust before asking for a single naira, we reduced drop-off at the most critical stage of the funnel.

Real value, upfront

Real value, upfront

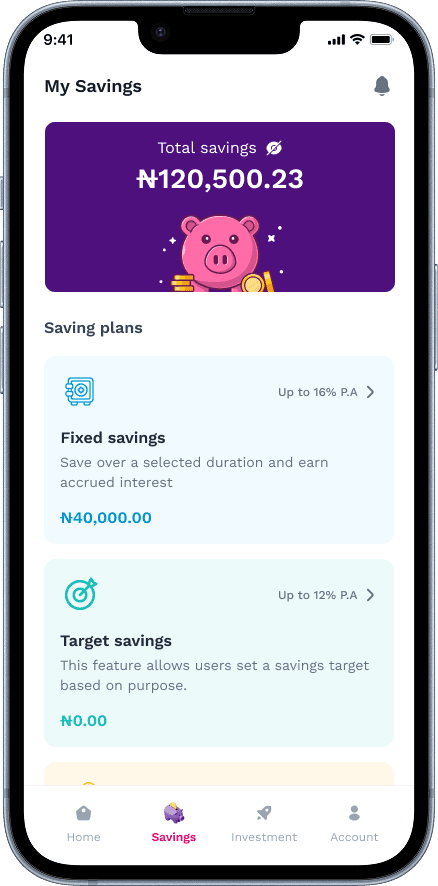

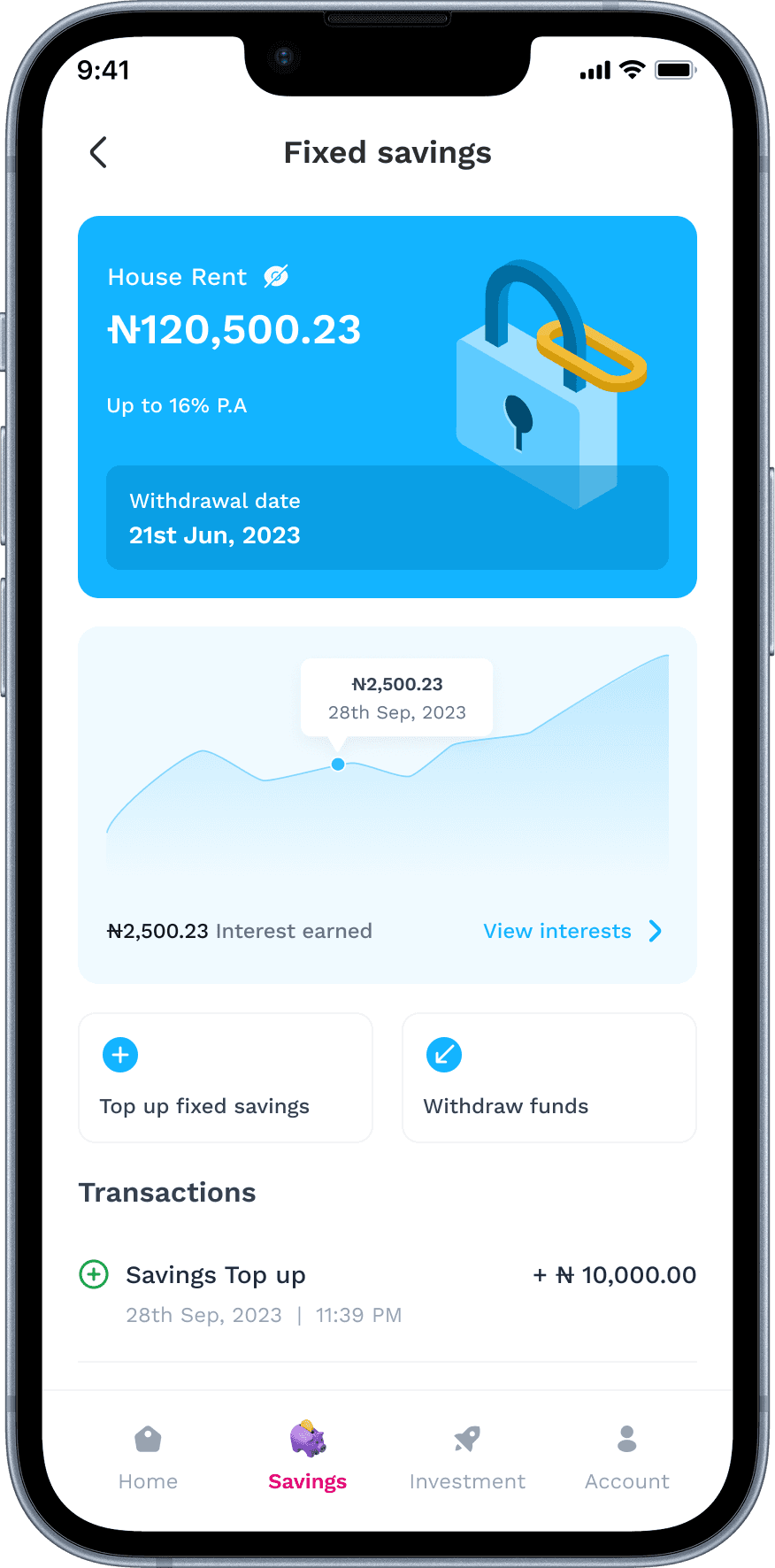

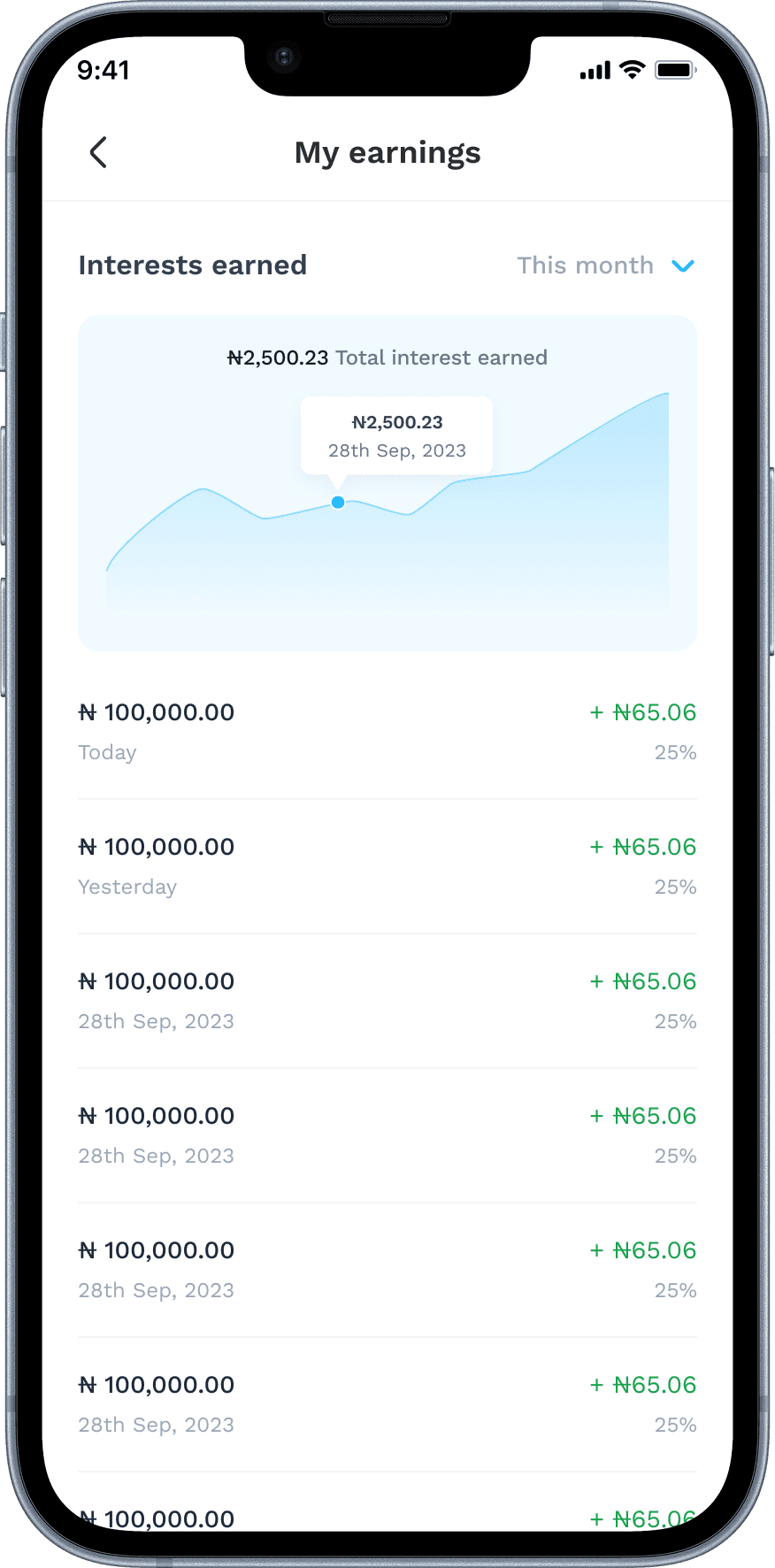

Interest rates were displayed prominently on the home screen, not buried in a product details page. We used large, high-contrast typography to make the returns feel real and tangible, giving users an immediate answer to “what’s in it for me?”

Interest rates were displayed prominently on the home screen, not buried in a product details page. We used large, high-contrast typography to make the returns feel real and tangible, giving users an immediate answer to “what’s in it for me?”

Built for irregular incomes

Built for irregular incomes

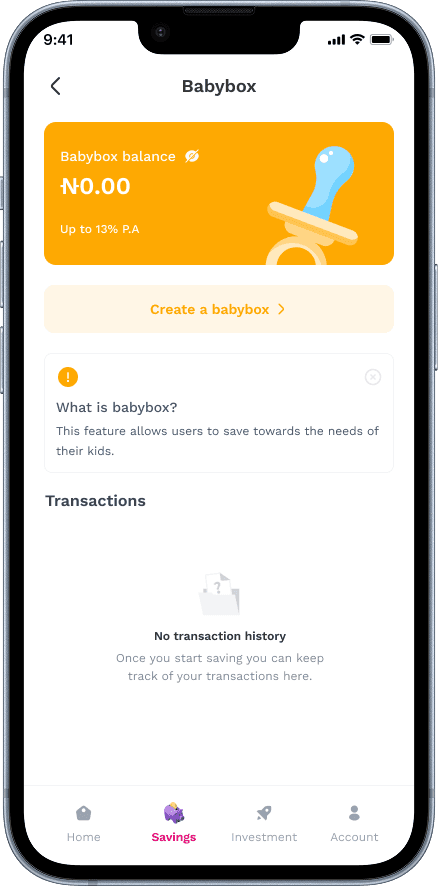

Rather than enforcing fixed monthly contributions, we designed a flexible savings model that lets users save any amount, at any time. The goal-setting flow uses a target amount rather than a monthly figure, which resonated far better with traders and freelancers.

Rather than enforcing fixed monthly contributions, we designed a flexible savings model that lets users save any amount, at any time. The goal-setting flow uses a target amount rather than a monthly figure, which resonated far better with traders and freelancers.

Simple, Encouraging Design

Simple, Encouraging Design

We kept the interface clean and easy with big buttons, one clear action at a time. Users saw their progress visually, with savings progress bars that filled up as they saved. And when they hit a milestone? We celebrated them. Nothing flashy, just thoughtful messages like “You’re doing well!”

We kept the interface clean and easy with big buttons, one clear action at a time. Users saw their progress visually, with savings progress bars that filled up as they saved. And when they hit a milestone? We celebrated them. Nothing flashy, just thoughtful messages like “You’re doing well!”

📊 The Results

📊 The Results

This wasn’t just about launching an app, it was about proving that design, when done right, can drive real change.

This wasn’t just about launching an app, it was about proving that design, when done right, can drive real change.

Metric Results

Metric Results

🧠 Designing for both sides

🧠 Designing for both sides

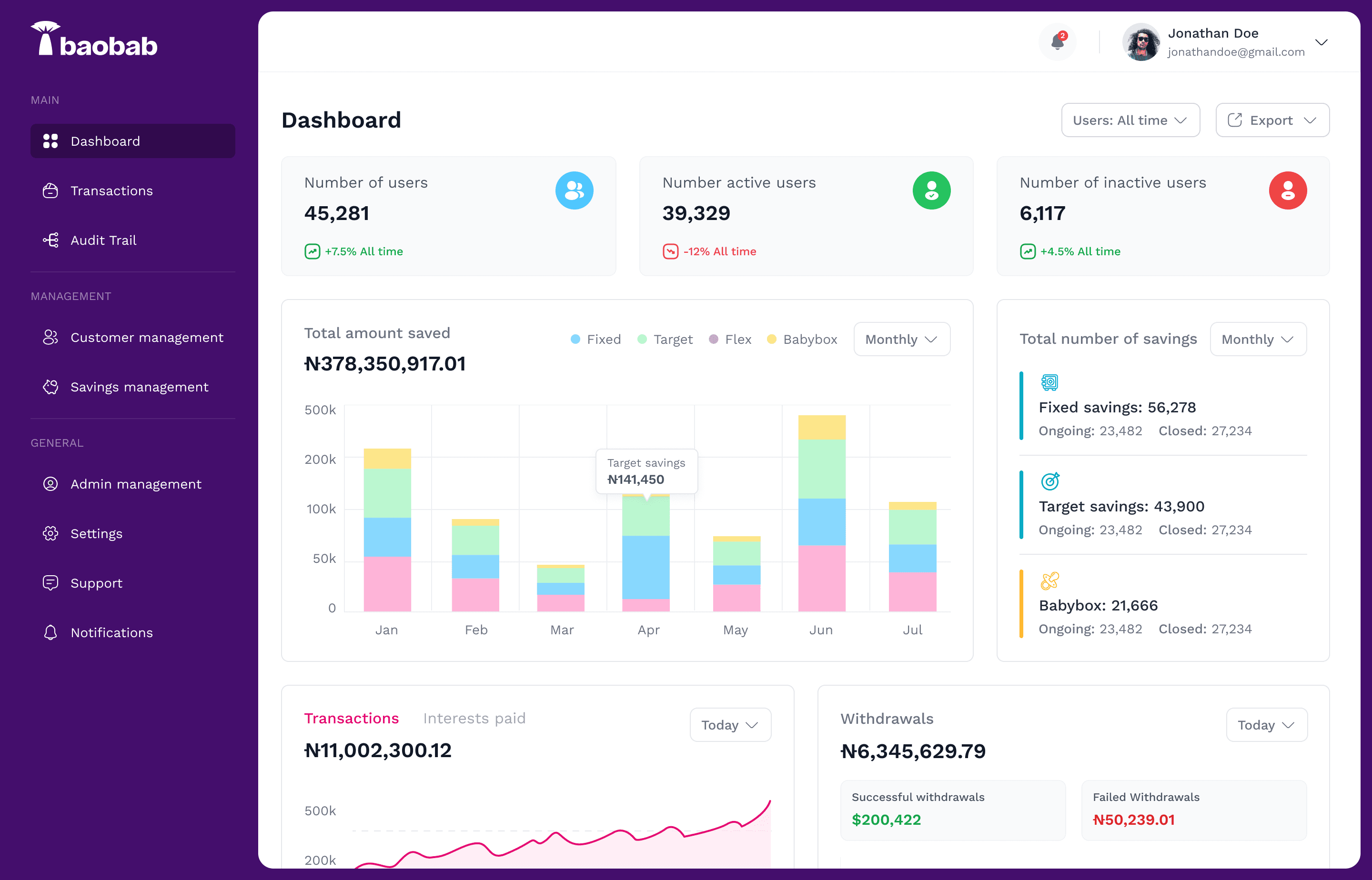

While the user-facing app was my primary focus, I also owned the design of the internal admin dashboard used daily by the Baobab operations team.

The admin experience had its own set of challenges: the team needed to monitor savings activity in real time, manage user accounts, approve withdrawal requests, and track interest disbursements, all without a dedicated engineering resource to build bespoke tooling.

I designed a clean, role-based dashboard with four core modules:

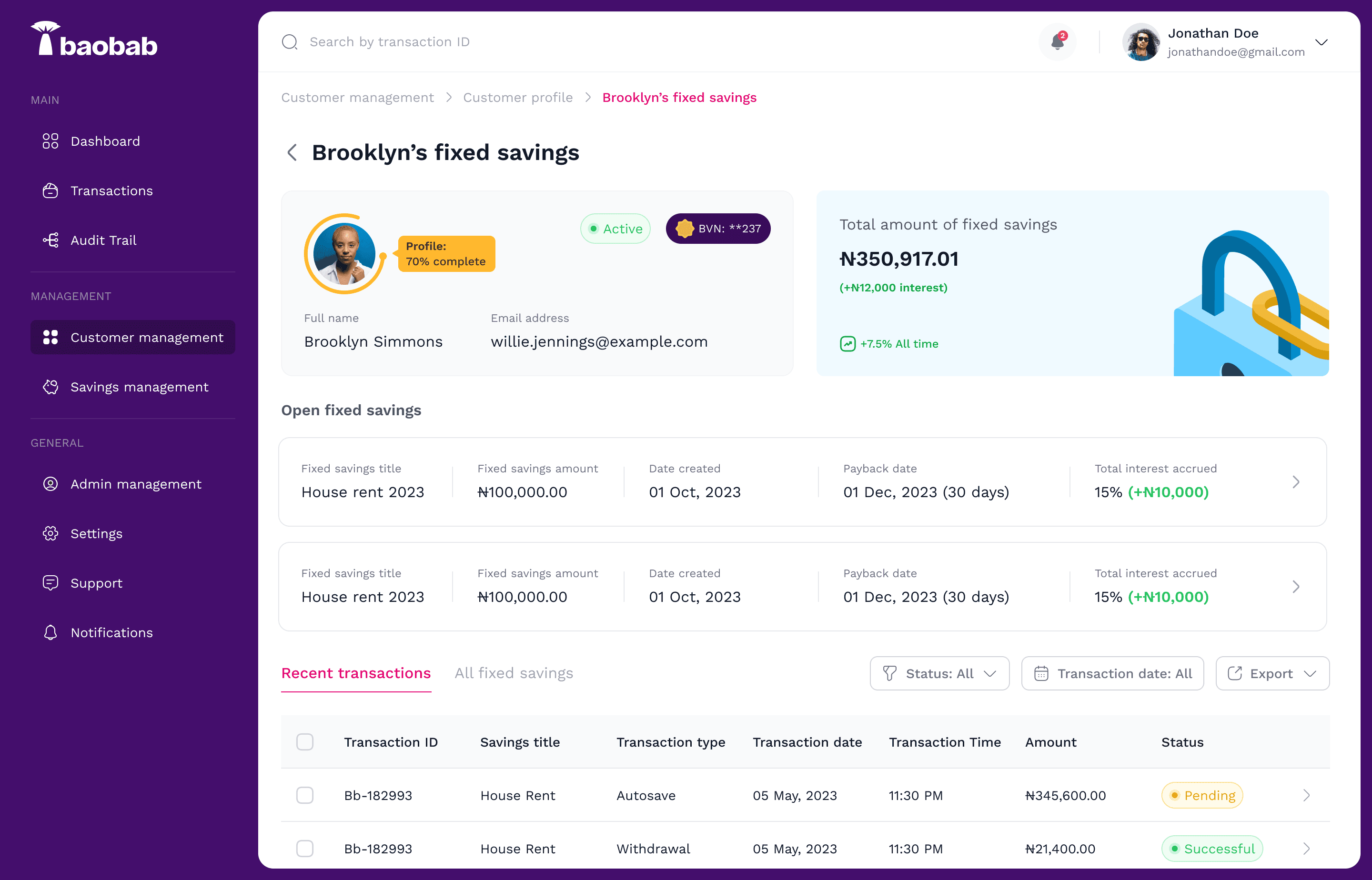

• Account Management: View, verify, and flag user accounts with full KYC status visibility.

While the user-facing app was my primary focus, I also owned the design of the internal admin dashboard used daily by the Baobab operations team.

The admin experience had its own set of challenges: the team needed to monitor savings activity in real time, manage user accounts, approve withdrawal requests, and track interest disbursements, all without a dedicated engineering resource to build bespoke tooling.

I designed a clean, role-based dashboard with four core modules:

• Account Management: View, verify, and flag user accounts with full KYC status visibility.

• Savings Overview: Real-time breakdown of active plans, total funds under management, and plan type distribution.

• Savings Overview: Real-time breakdown of active plans, total funds under management, and plan type distribution.

• Interest Disbursement: A queue-based tool for reviewing and approving scheduled payouts, with audit logs.

• Interest Disbursement: A queue-based tool for reviewing and approving scheduled payouts, with audit logs.

• Reporting: Exportable summaries for weekly ops reviews and regulatory reporting.

• Reporting: Exportable summaries for weekly ops reviews and regulatory reporting.

The guiding principle was the same as the consumer app: reduce cognitive load. Every screen was designed to answer one clear question, so the team could act quickly and confidently.

The guiding principle was the same as the consumer app: reduce cognitive load. Every screen was designed to answer one clear question, so the team could act quickly and confidently.

🚧 Challenges & What I’d Do Differently

🚧 Challenges & What I’d Do Differently

Every project has its friction, and Jollof+ was no different.

Every project has its friction, and Jollof+ was no different.

Timeline Pressure

Timeline Pressure

Delivering a production-ready MVP in 12 weeks meant making hard calls about scope. Several features, including a referral programme and a savings streak tracker, were deprioritised to protect launch quality. I’d have advocated earlier for a phased roadmap to set clearer stakeholder expectations from the start.

Delivering a production-ready MVP in 12 weeks meant making hard calls about scope. Several features, including a referral programme and a savings streak tracker, were deprioritised to protect launch quality. I’d have advocated earlier for a phased roadmap to set clearer stakeholder expectations from the start.

Accessibility Gaps

Accessibility Gaps

In retrospect, I’d invest more time in low-vision and screen-reader testing. Our usability sessions focused on task completion, but didn’t cover assistive technology users, a gap I want to close in future fintech work.

In retrospect, I’d invest more time in low-vision and screen-reader testing. Our usability sessions focused on task completion, but didn’t cover assistive technology users, a gap I want to close in future fintech work.